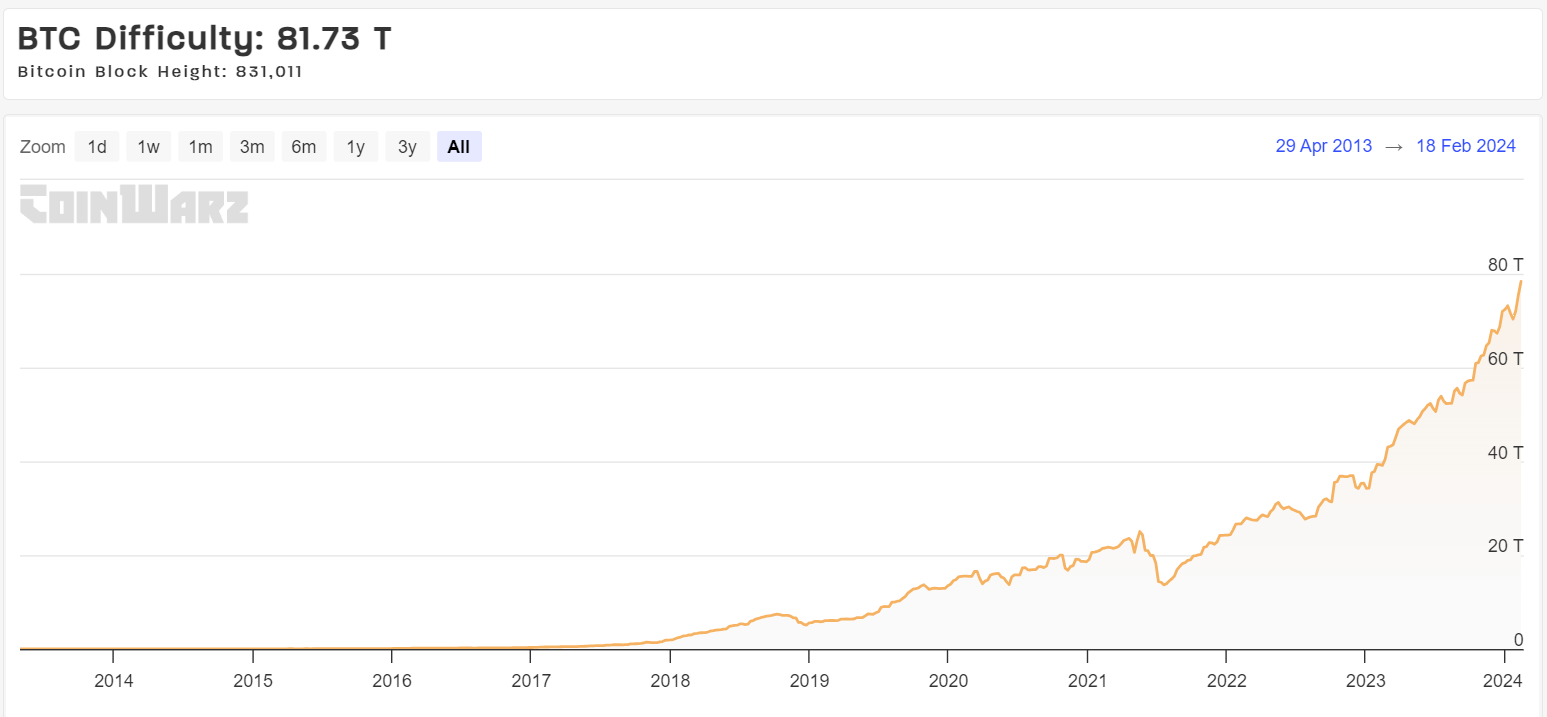

Bitcoin’s price surged by 155% from its low point at the end of 2022, closing the year at $42,217. This increase was largely fueled by expectations of a spot Bitcoin ETF approval, the recovery from the aftermath of FTX’s collapse, and several high-profile bankruptcies in late 2022. Additionally, the introduction of the ordinals protocol and inscriptions spurred a 336% year-over-year jump in transaction fees, contributing to the growth of web3 applications and Bitcoin tokenization. These developments, coupled with the arrival of more efficient ASIC mining machines, propelled a 104% increase in network difficulty. Yet, the hashprice, a measure of mining profitability, still ended the year on a high note, reflecting a 57% improvement.

The global Bitcoin hashrate experienced diversification, with significant contributions from the Middle East, South America, Bhutan, China, and Russia. In anticipation of Bitcoin’s fourth halving, major mining operators have been strategically acquiring advanced ASICs through equity financing. This move aims to enhance their mining fleet’s size and efficiency.

Despite the network’s growing difficulty, miners have adapted by focusing on acquiring newer, more efficient mining equipment. Over the year, public mining companies invested over $1.53 billion in machinery, amassing more than 94 EH of mining power. These acquisitions have positioned miners favorably as they prepare for the network halving, an event expected to sideline 15-20% of the network’s hashrate due to profitability concerns.

New Challenges in 2024

Looking ahead to 2024, the Bitcoin mining sector must brace for increased hashprice volatility. This fluctuation will stem from varying demands for block space, leading to sharp changes in transaction fees and, consequently, the hashrate. With transaction fees making a significant leap in 2023, miners are exploring new risk management strategies to stabilize revenue. These include the adoption of hashrate derivatives contracts, aiming to maintain revenue predictability and investor confidence amidst the uncertainties.

In 2023, the stabilization of global mining power costs, especially in the U.S., provided a stable backdrop for miners. This stability was attributed to high U.S. natural gas production, surplus inventories, and reduced demand due to milder temperatures and a slight decline in industrial consumption. As the industry gears up for the halving event, these factors are crucial for sustaining operations in a volatile market

Network Growth

The Bitcoin network saw a significant increase in transaction fees, accumulating 23,445 BTC over the year—more than four times the amount in 2022. This spike was driven by the growing interest in BRC-20 tokens, particularly noted in May, November, and December, due to the Ordinals transactions. The network’s difficulty and hashrate also experienced remarkable growth, with the latter doubling to 515 EH. This growth was powered by several developments, including the introduction of new, more affordable ASICs, lower natural gas prices, and an influx of international hashrate.

Mining efficiency received a boost from technological advancements and strategic operational adjustments. The deployment of new ASIC models at competitive prices, such as the M50 and M60 series, played a crucial role. Additionally, the decrease in natural gas prices contributed to a more favorable operating environment for miners. The energy market’s stability, particularly in natural gas, contrasted sharply with the previous year’s volatility, providing a steadier cost basis for mining operations.

In 2023, the hashprice, an essential metric for miners, fluctuated between $0.06 and $0.10 for most of the year, briefly deviating from this range due to variations in transaction fees and network difficulty. The stability in energy prices, especially natural gas, contributed significantly to the mining industry’s resilience. The U.S., hosting a substantial portion of the global hashrate, benefited from high natural gas production and increased inventories, ensuring a steady energy supply despite fluctuating demands.

Regulatory Changes

Texas emerged as a battleground for cryptocurrency mining regulation with the introduction of Bill 1929 in early 2023. This law, effective from September 1, mandates that large-scale virtual currency mining operations in the ERCOT region must register due to their substantial power needs. This move aims to streamline the integration of mining activities with the state’s power grid, ensuring stability and efficiency.

Conversely, Bill 1751, which sought to exclude miners from grid balancing programs, did not advance beyond the Committee on State Affairs. The proposal marked a pivotal moment, stirring industry debate over the role of miners in energy markets. Despite its failure, the bill underscored the potential for legislative challenges to the sector.

Federal Developments and International Trends

On the federal front, the Biden Administration’s initial proposal of the Digital Asset Mining Energy (DAME) Tax represented a significant potential burden on Bitcoin mining operations. However, the removal of this tax from the budget was a notable victory for the industry, illustrating the effectiveness of advocacy and dialogue in shaping policy.

Further enhancing the financial landscape for miners, new Financial Accounting Standards Board (FASB) rules set to take effect in 2025 will allow companies to report Bitcoin holdings at fair value. This change is poised to benefit miners with significant Bitcoin reserves by more accurately reflecting their assets’ worth, thereby enhancing net income figures.

Senator Elizabeth Warren’s push to extend the Bank Secrecy Act to include Know-Your-Customer (KYC) requirements for miners represents another layer of regulatory evolution, emphasizing the importance of transparency and anti-money laundering efforts in the sector.

Internationally, Russia’s move to categorize Bitcoin mining as akin to natural resource extraction showcases a global shift towards recognizing and integrating cryptocurrency into economic frameworks. Such policies not only validate the industry but also position countries like Russia as attractive alternatives for mining operations seeking regulatory clarity and support.

Optimism Grows Amidst Regulatory Evolution

Reports and analyses from reputable sources, including KPMG, the Financial Times, and Bloomberg Intelligence, have contributed to a more nuanced understanding of Bitcoin’s environmental implications. These perspectives highlight the potential for mining to align with renewable energy initiatives and grid balancing efforts, challenging the previously dominant narrative of environmental detriment.

The emergence of new mining pools, such as OCEAN and DEMAND, reflects a technical and philosophical evolution towards decentralization. Leveraging StratumV2, these pools offer miners a greater role in block template creation, promoting transparency and autonomy. However, regulatory considerations, particularly related to KYC and anti-money laundering, may limit widespread adoption of such innovations.

Market Shifts

Public miners demonstrated a cautious approach to Bitcoin (BTC) sales throughout 2023. This change of pace contrasts sharply with the aggressive holding pattern observed during the bull market peaks of 2021 and the subsequent selling pressures of 2022. Notably, despite the allure of BTC price increases and intermittent fee surges last year, these entities opted to sell less BTC. The financial landscape for these miners has notably evolved; they now employ a more balanced treasury management strategy, carefully navigating between holding onto their BTC assets and liquidating them for cash.

This strategic pivot is largely attributed to the improved mining economics witnessed in the latter half of 2023, buoyed by narratives surrounding ETFs and Bitcoin’s halving event. The updated guidance from the Financial Accounting Standards Board (FASB) further bolsters this trend, allowing miners to report BTC holdings at their fair market value, thus potentially increasing their propensity to hold.

Hashrate Dynamics and Geographic Shifts

The 2022 crash was particularly pronounced in the initial months of 2023, leading to a reduced emphasis on growth and an involuntary ceding of hashrate dominance to miners outside North America. However, the latter half of the year marked a turning point, with mining economics on the rise and a renewed interest in mining equities, thus re-establishing North American miners’ competitive edge in the global mining landscape.

The ASIC investment landscape in 2023 tells a story of cautious optimism evolving into strategic expansion. The year started with miners prioritizing the activation of previously ordered ASICs amidst a challenging capital environment. Yet, as the year progressed, particularly in its final quarter, a wave of large ASIC purchase announcements signaled a robust confidence boost, driven by an improving outlook on equity markets and anticipation surrounding the Bitcoin ETF’s approval.

Public miners collectively raised over $1.1 billion in equity capital through the first three quarters, a figure expected to climb as Q4 data emerges. This strategic capital influx contrasts starkly with the mere $44 million raised through debt, highlighting the sector’s shift away from debt financing towards equity-based growth strategies.

With the Bitcoin halving event on the horizon in early Q2, the focus has sharply turned towards enhancing mining efficiency, specifically through upgrades to more energy-efficient machinery and infrastructure expansion. This push for efficiency is underscored by the substantial investment in state-of-the-art mining equipment, totaling more than $1.53 billion over the year. The latter half of 2023 alone saw a 59.3% increase in purchase orders, emphasizing the industry’s commitment to cutting-edge technology and efficiency.

The early trends of 2024 further cement this strategic direction, with over $393 million already invested in high-efficiency mining machines. Leading this charge are CleanSpark and Pheonix, setting a competitive pace for the industry.

Bitcoin Blockspace Demand

The introduction of Ordinals and other novel token standards has reshaped the demand for Bitcoin blockspace. This shift has led to increased volatility in transaction fees and mempool congestion, highlighting the delicate balance required to maintain sustainable fee levels for miners amidst declining BTC issuance.

The year 2023 witnessed a notable rise in transaction fees, with spikes exceeding 25% of total block rewards. This surge has crucial implications for Bitcoin miners, for whom transaction fees represent a significant portion of revenue, especially post-halving.

A New Era for Bitcoin Mining

To counteract the uncertainty brought by fee volatility, the mining sector may lean towards further financialization, including the development of blockspace futures and transaction fee forwards. These instruments could offer miners a hedge against fee fluctuations, potentially bringing in a new breed of miners who operate on an opportunistic basis, akin to Texas miners exploiting power market variations.

The coming year promises further innovation, potentially transforming Bitcoin into a prime settlement layer for various economic activities, including NFTs, DeFi, and stablecoins. Among the anticipated developments are Taproot Assets, enabling on-chain NFT and asset creation with seamless off-chain interoperability through the Lightning Network. This could significantly bolster Bitcoin’s position against competing chains by facilitating low-cost, instant transactions.

Additionally, new token standards like Runes and the CBRC token standard are set to enhance the efficiency of token issuance and transfer, potentially increasing the economic density of Bitcoin blocks. The introduction of Covenants and innovative protocols like BitVM and discreet log contracts (DLCs) could further solidify Bitcoin’s role in the smart contract arena, competing directly with other blockchains.

The industry must also prepare for emerging challenges, such as sophisticated forms of miner extractable value (MEV). Instances like Sophon’s mint killer bot and PSBT front-running highlight the need for vigilance and adaptation to protect the integrity of transactions and mining operations.

Replace-By-Fee on Bitcoin’s Mempool Dynamics

The Replace-By-Fee (RBF) mechanism has emerged as a pivotal tool for users to navigate the congested mempool, especially in scenarios where transaction fees surge unexpectedly. RBF enables Bitcoin users to adjust the fee of an already broadcast transaction. This strategic move not only accelerates the confirmation process but also significantly enhances miners’ incentives to prioritize these transactions for block inclusion.

The unpredictability in transaction fees has made it challenging for users to set appropriate feerates, leading to a noticeable uptick in the adoption of RBF. This trend is anticipated to reshape mempool activities by driving feerates higher and, consequently, increasing miners’ revenue. Typically, a replaced transaction’s feerate is marked up by 20% to 50% over the original, making it an attractive proposition for miners.

Transaction Acceleration

Beyond RBF, the cryptocurrency ecosystem has seen the emergence of Transaction Accelerators. These services, offered by entities like Binance and Mempool.Space, provide a straightforward mechanism for users to ensure their transactions are included in the upcoming block. By allowing payments directly to pools through off-chain methods, including fiat and BTC, these accelerators circumvent traditional mempool queuing. Although these transactions do not directly contribute to the block’s total rewards, they significantly bolster miners’ earnings.

The reliance on such accelerators shows the increasing competition for block space and the challenges in predicting optimal feerates. As the landscape of transaction fees grows more complex, the role of Out-Of-Band (OOB) transactions in generating revenue for miners is expected to expand. This shift is part of a broader trend towards the financialization of block space, with RBF transactions poised to command a larger share of transaction fees in 2024.

Reports reveal that RBF transactions contribute between 10% and 20% of the total transaction fees under standard mempool conditions. However, this figure soared to 50% during periods of low fees in September 2023. With the upcoming halving, which will see transaction fees doubling as a portion of block rewards, the incentive for miners to support RBF by operating Full RBF nodes is set to increase. Research indicates that as of August 2023, 31% of the hashrate, spread across at least four pools, was committed to mining Full RBF, a number that may have climbed to 70% by January 2024.

Mempool Efficiency and User Experience

The proposal of “One-Shot Replace-By-Fee” by developer Peter Todd is set to further incentivize miners to adopt Full RBF. This new approach aims to refine the RBF mechanism by ensuring that replacements elevate transactions to the top of the mempool, facilitating immediate block inclusion. Such innovations underscore the evolving strategies to manage high-time preference transactions, thereby dictating the competitive landscape for transaction fees.

Looking ahead, the development of mempool-centric proposals like Cluster Mempools, Package Relay, V3 transaction relay, and Ephemeral Anchors promises to equip users with more sophisticated tools to navigate fee volatility. These advancements will not only help users secure optimal feerates but also benefit miners by enabling the creation of more efficient block templates.

Blocktimes and Transaction Fees

Recent studies have revealed a significant connection between the timing of Bitcoin block generation and the transaction fees, commonly referred to as feerates. This relationship is crucial, especially as the cryptocurrency world anticipates the halving event, which could potentially slow down the rate at which miners produce new blocks. This slowdown could affect miners’ profitability and could increase the transaction fees due to heightened fee pressures.

Historically, the Bitcoin network has aimed for a block generation time of 10 minutes. However, data from the last three years shows an average blocktime of 9 minutes and 51 seconds. This acceleration in block production has been linked to a 262% increase in mining difficulty during the same period, suggesting a complex interplay between blocktimes, mining difficulty, and transaction fees.

To delve deeper into this relationship, a correlation and regression analysis was conducted on data spanning from December 2015 to January 2024. This analysis confirmed that as blocktimes deviate from the 10-minute mark, transaction fees tend to adjust accordingly. Specifically, for every minute under 15 minutes that a block is produced early, transaction fees decrease by approximately 2.2 Sat/vByte per minute. Conversely, for every minute over 15 minutes, fees increase by 0.71 Sat/vByte per minute.

Mining Revenues

The upcoming halving event, where block rewards for miners are cut in half, is anticipated to lower the network hashrate temporarily as less profitable miners cease operations. This reduction in hashrate could lead to longer blocktimes, putting additional pressure on transaction fees. If 20% of the network hashrate goes offline, blocktimes could increase by an average of 20% until the difficulty adjusts to stabilize block production times.

This potential increase in blocktimes could have a noticeable impact on miners’ revenues from transaction fees. For instance, during high fee periods, an 8% increase in transaction fees could result in significant additional income for miners. However, if blocktimes decrease, this could conversely reduce transaction fee income by about 2%, focusing solely on the impact of hashrate on fees.

Moreover, the intricate balance between block subsidy and transaction fees becomes more pronounced. While shorter blocktimes could reduce transaction fees, the increased frequency of block generation could offset this loss by providing miners with more block rewards over the year. This dynamic suggests that miners could actually see an increase in revenue, despite the potential for lower transaction fees.

In 2024, with the halving and other factors such as increased Replace-By-Fee (RBF) usage and inscription activities, the cryptocurrency community may witness a surge in fee pressures and volatility. This period will likely be a critical test of the network’s resilience and the adaptability of miners and users alike.

Energy Strategies for Crypto Miners

The breakeven revenue for miners varies widely depending on their fleet efficiency and the hashprice. Currently, the hashprice stands at $0.082, but this could fall to $0.045 post-halving. For a miner with a 30 J/TH fleet efficiency, energy prices need to stay below $63/MWh to maintain a positive gross profit. This situation underscores the need for miners to carefully manage their energy costs, especially in the face of fluctuating prices.

Miners face the challenge of deciding how much of their capacity to hedge against fluctuating energy prices. Hedging allows miners to manage energy price volatility and maintain operational profitability. However, it also comes with the risk of locking in a fixed hedge price that might exceed the marginal breakeven point if spot power prices settle lower. For instance, hedges for load zone West in ERCOT for the months following the April 2024 halving have peaked at around $80/MWh. Miners with a machine efficiency of up to 35 J/TH would need the hashprice to settle at more than $0.07 to stay profitable under these conditions.

Machine Efficiency

Studies also reveal the critical role of machine efficiency in maintaining profitability post-halving. Miners with newer generation machines, like the S21s, can withstand lower hashprices due to their improved efficiency. This highlights the importance of investing in efficient mining equipment to enhance gross margins and ensure profitability in a more challenging post-halving environment.

Similar to traditional commodity production industries, Bitcoin mining can benefit from hedging strategies. These strategies offer miners a way to manage the increased volatility expected from the upcoming halving, especially concerning the reliance on transaction fees. Hedging allows for more predictable revenue streams by locking in prices or production costs, providing a cushion against the unpredictable nature of mining rewards.

Adopting hedging strategies enables miners to secure a portion of their revenue, enhancing predictability and stability in their operations. By hedging both power costs and coin production, miners gain a greater degree of control over their cost structures, helping to navigate the uncertainties of the mining landscape more effectively. This approach not only aids in managing operational costs but also in maintaining profitability during periods of market volatility.

Capital Access and Shareholder Value

For public mining companies, demonstrating stability through effective hedging strategies can significantly impact shareholder value. Stable cash flows and clear visibility into financial health can attract more investment and support expansion efforts. In a market where public mining stocks are influenced by a myriad of factors, showcasing a commitment to prudent risk management can differentiate a miner in the eyes of investors.

The strategic use of hashrate derivatives presents an opportunity for miners to capitalize on transaction fee volatility. By locking in production rates during peak transaction fee periods, miners can maintain high levels of production even if fees decrease. This approach allows miners to navigate the inherent volatility in transaction fees, potentially unlocking additional revenue streams.

Despite their advantages, derivative products for mining are not without their challenges. The complexity of these contracts, particularly the distinction between cash-settled and physically settled options, introduces significant counterparty risks. The market for such products is currently limited, reflecting the challenges in pricing and liquidity. However, as the industry evolves, these financial instruments could play a crucial role in the risk management strategies of miners.

Bitcoin Mining Industry Evolution

Miners pursued more efficient energy strategies and integrated vertically to minimize or eliminate extra costs associated with hosting services. This move not only aimed at enhancing operational margins but also at adjusting to the evolving dynamics of the cryptocurrency mining landscape.

In an industry where electricity costs are crucial, Bitcoin miners have been compelled to innovate their business models. Many have shifted towards vertical integration, a strategy aimed at reducing operational costs by taking control of energy sources and infrastructure. This integration allows miners to lower their position on the cost curve, making them more resilient against hashprice volatility, which is expected to escalate due to various factors, including the halving event and the influence of spot Bitcoin ETFs on the market.

The hosting business within the mining industry is also undergoing transformation. Hosting providers are now reevaluating their contract structures to ensure they align more closely with the miners’ cash flow, particularly those operating older machine fleets. The new model leans towards cash flow splits and energy curtailment agreements, offering a more flexible approach that benefits both miners and hosting providers in times of fluctuating hashprices.

High-Performance Computing

Amidst a challenging environment characterized by low hashprices and a scarcity of capital for expansion, several Bitcoin miners ventured into High-Performance Computing (HPC) in 2023. This pivot aimed at diversifying revenue streams and tapping into new capital sources, especially from the booming AI sector. The transition, however, is not straightforward. HPC data centers demand more intricate designs, including advanced networking structures and stringent cooling requirements, to optimize performance and minimize downtime.

The financial and operational models of HPC ventures differ significantly from traditional bitcoin mining operations. Some miners have opted to partner with Cloud Service Providers (CSPs) for easier management and stable cash flows, while others have taken the more complex route of developing their own cloud platforms. This latter approach requires substantial investment in hardware, software, and team expansion but promises higher returns by directly serving end clients.

For those who have heavily invested in HPC, the challenge will be to balance the potential of this new venture against the core business of mining. The success of the HPC model will largely depend on the execution of construction, design, operations, and finance strategies while navigating supply chain challenges and capitalizing on the demand for AI and other high-compute applications.

Bitcoin ETFs

The financial world has witnessed a paradigm shift with the introduction of Bitcoin Exchange-Traded Funds (ETFs), offering investors a direct route to the bitcoin market. This development has significantly impacted the traditional avenues of investment, particularly public mining stocks, which previously served as a primary method for investors to leverage bitcoin’s price movements. This article delves into the short-term and long-term effects of Bitcoin ETFs on public miners and explores the evolving strategies in mergers and acquisitions (M&A) within the mining sector.

In the immediate aftermath of Bitcoin ETF approvals, the investment community is reevaluating the appeal of public mining stocks. Retail investors, historically viewing these stocks as a means to indirectly invest in bitcoin, now compare them against the performance of Bitcoin ETFs. Meanwhile, institutional investors display a tendency to favor Bitcoin ETFs for long positions while adopting a bearish stance on mining stocks. This trend, gaining momentum since the start of 2024, underscores a strategic shift in investment preferences.

Long-Term Challenges and Opportunities

Looking ahead, public miners face stiff competition from Bitcoin ETFs. To attract savvy investors, miners must justify their value proposition beyond mere exposure to bitcoin. The key to differentiation lies in their ability to generate substantial free cash flow, reflecting a direct correlation between a miner’s financial health and its stock performance. Miners with lower operational margins and a history of poor capital returns may struggle to raise equity, especially if they cannot prove their potential for high returns on investment. Conversely, those demonstrating robust financials could mitigate the competitive pressures of Bitcoin ETFs, potentially gaining inclusion in a wider array of investment products and benefiting from increased market research and coverage.

As the mining industry adapts to these changes, M&A activities emerge as strategic maneuvers to enhance operational efficiency and financial stability. The evolving dynamics, influenced by the forthcoming halving event in 2024, have propelled miners to explore mergers and acquisitions for a variety of strategic benefits.

Response to Market Dynamics

Miners are increasingly inclined towards M&A to address challenges such as high operational costs and the need for compelling growth narratives. The objective is to achieve vertical integration, reduce dependencies on external factors, and secure capital in a more favorable mining economy. The shift towards M&A partly comes from the improved mining economics, attributed to higher transaction fees and a favorable performance of bitcoin, coupled with reduced energy costs due to low natural gas prices. These factors have considerably enhanced the gross mining margins compared to early 2023.

The M&A landscape in 2024 could have significant activity, with public miners of smaller market caps being attractive targets for larger entities. The goal is to achieve cost efficiencies, enhance operational control, and navigate the challenges posed by the halving event. Moreover, the acquisition of turnkey sites ready for new hashrate deployment presents a strategic opportunity for miners to expand their operations efficiently. This approach is particularly appealing given the constrained capacity at existing sites and the lengthy timelines for energizing new locations.

Anticipating the Impact of Bitcoin Halving

Coinmetrics’ recent analysis reveals that certain mining machines, namely M20S, M32, S17, A1066, A1246, and S9, contribute 98 EH (Exahashes) to the current network hashrate of approximately 515 EH. This article delves into the potential repercussions of the halving on mining efficiency and the broader industry landscape.

Mining operations are bracing for the halving event, which traditionally impacts the economics of Bitcoin mining by reducing the block reward. The halving could lead to a significant portion of the network’s hashrate going offline, particularly affecting older and less efficient ASIC (Application-Specific Integrated Circuit) models. Analysis indicates that 15 to 20% of the network’s hashrate, equating to 86 to 115 EH, might be at risk due to the decreased profitability of these machines in the post-halving environment.

To estimate this impact, we analyzed the breakeven point for various ASIC models, considering the expected post-halving block subsidy of 3.125 Bitcoins and assuming transaction fees contribute to 15% of mining rewards, with a Bitcoin price fixed at $45,000. This assessment also took into account future power prices and costs from publicly known mining operations.

Changes in Mining Operations

Miners are adapting to these challenges by employing strategies such as custom firmware upgrades to enhance ASIC efficiency and, therefore, improve their operational breakeven points. Additionally, rather than exiting the network, some miners with outdated ASIC models may transfer their operations to regions offering lower electricity costs, thereby sustaining their competitive edge.

The industry is also witnessing a trend where miners operating with less efficient machines, such as the S17 models, are upgrading to more advanced and efficient models like the S19s or S19j Pros. This shift not only ensures the sustainability of mining operations but also enhances overall network efficiency.

The year 2023 marked a period of recovery and expansion within the mining sector, characterized by higher Bitcoin prices, increased transaction fees, and reduced energy costs. These factors collectively led to improved profitability and operational margins, despite the doubling of network hashrate.

As the halving draws near, miners are leveraging improved market liquidity and demand to finance new infrastructure developments and acquire more efficient ASIC models, such as the T21, S21, and M60 series. This proactive approach could maintain, if not increase, the network’s hashrate.

Moreover, the industry may experience heightened merger and acquisition activities among private mining operators as they strive to optimize their operations in anticipation of the changing economic landscape post-halving. Transaction fee volatility remains a critical variable, potentially influencing hashprice, mining difficulty, and block time variations, which could further affect mining pool payout structures and strategic decision-making.

2024 marks an important year for cryptocurrencies. Adoption is imminent, and Bitcoin could increase its dominance in financial markets. Despite potential volatility, the industry leans into hedging and high-performance computing to diversify and stabilize revenues. As the halving approaches, Bitcoin’s ecosystem continues its road to redefining finance and technology.

Takeaways

- Bitcoin’s price increased by 155% due to ETF expectations, FTX recovery, and ordinals protocol introduction.

- Transaction fees jumped 336%, driven by interest in Bitcoin tokenization and web3 applications.

- Mining network difficulty soared by 104%, but mining profitability improved by 57%.

- Global Bitcoin hashrate diversified, with strategic ASIC acquisitions by miners for the upcoming halving.

- 2024 foresees hashprice volatility, pushing miners towards risk management strategies like hashrate derivatives.

- Transaction fee spikes in 2023 prompted a significant increase in Bitcoin network activity.

- Texas regulated cryptocurrency mining, mandating large operations to register due to power needs.

- The Biden Administration removed a proposed tax on Bitcoin mining, boosting the industry.

- Miners adapting to lower hashprices post-halving by investing in efficient mining equipment.