The digital world is a continuously growing industry, and it seems that it has no intention to stop. Blockchain technology, and innovation in digital currency, are also growing rapidly; proving themselves as limitless more and more each day. This technology’s initial goal was to decentralize transactions and keep a record of them through timestamps, making the data stored in a blockchain network virtually impossible to manipulate.

However, as time goes by, people keep experimenting with this technology; and these experiments keep leading us to new findings of what blockchain technology has to offer. One of these innovations, if we may say, is Non-Fungible Tokens also known as NFTs. Its inventors aim to introduce the world of blockchain technology to the world of art through NFTs, using the technology to preserve the uniqueness of digital art pieces. Throughout this article, we will mainly discuss NFTs, how they work, what is their purpose, and how to create one of your own.

What are NFTs?

To begin with, NFTs were invented by digital artist Kevin McCoy and tech entrepreneur Anil Dash in 2014. The first-ever NFT that was minted went by the name of ‘Quantum’ and it features a pixelated octagon that changes colors like an octopus. Most of NFTs are stored on the Ethereum network mainly because of their programmability; however, there are other smaller networks that support NFTs too.

As mentioned before, NFT is short for Non-fungible tokens; non-fungible stands for the uniqueness that every NFT has and the fact that they aren’t replaceable. In other words, an NFT is a token that is unique and cannot be replaced. Most cryptocurrencies are fungible, meaning that you can trade them with one another – an example would be trading one Ethereum for another Ethereum and so on. An NFT, on the other hand, is a one-of-a-kind asset, making it impossible to trade NFTs with one another.

These tokens can be used to represent ownership of unique items and they let us tokenize nearly everything that can be owned – with a basic example being digital art and music. We should also mention that people have started listing real estate as NFTs lately, making the use of NFTs even broader.

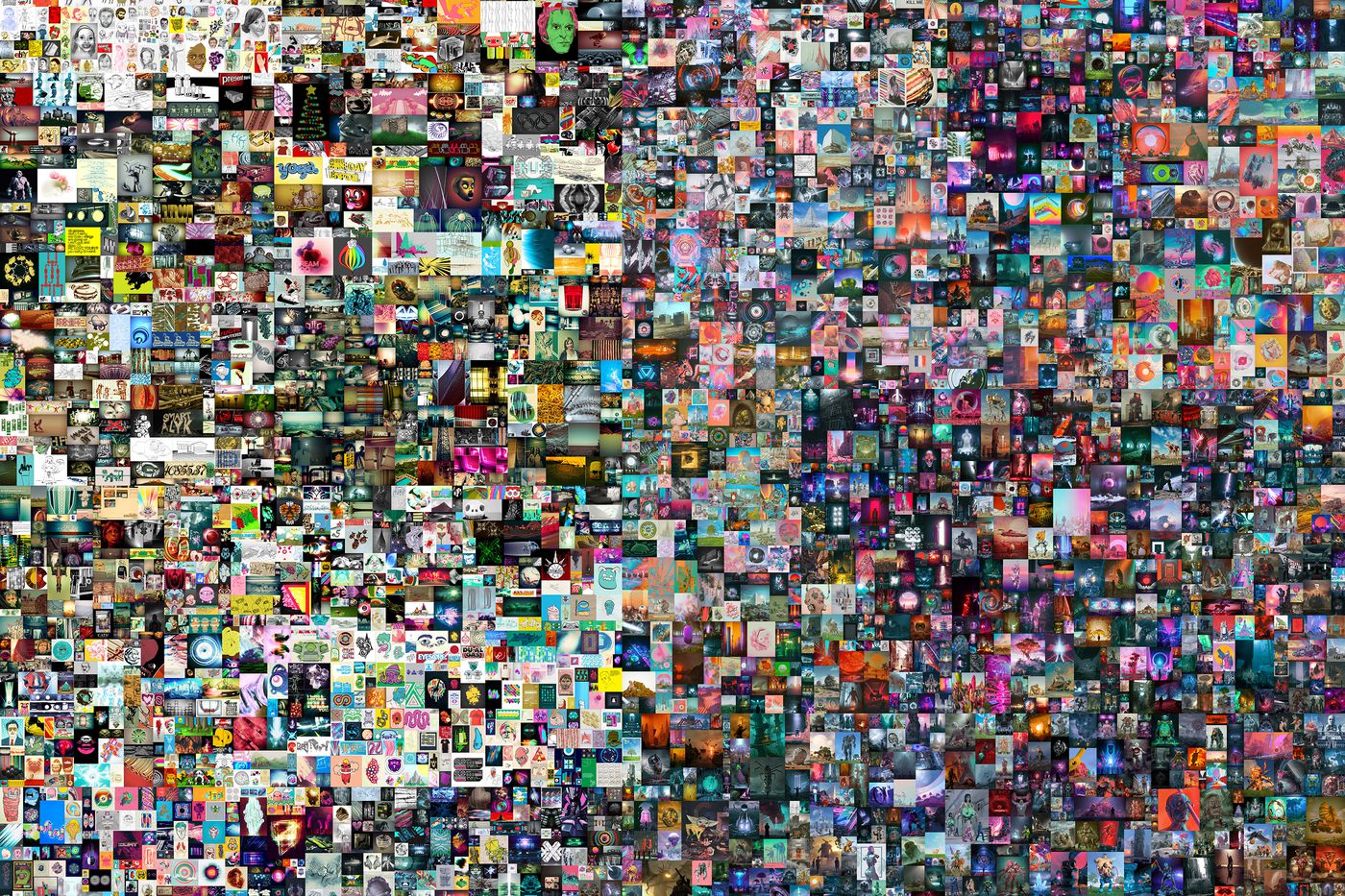

This crypto art market did not have that much attention until 2017, and it was mainly in 2021 that people truly started to show interest for it. This meant people paying millions for digital pieces of art – some being classic memes while some being collectible cards. By April 2021, more than $2 billion have flown through this market on the first quarter of this year; with some NFTs being sold for tens of millions of dollars.

Here is a list of some NFTs that were sold with a price above that of $1 million:

| Everydays – The First 5000 Days | $69.3 million |

| Hashmasks | $16 million |

| CryptoPunk #3100 | $7.58 million |

| CryptoPunk #7804 | $7.57 million |

| Crossroads | $6.6 million |

| Grimes artwork/music videos | $6 million |

| First Twitter Tweet | $2.9 million |

| CryptoPunk #6965 | $1.6 million |

| Axie Infinity Virtual Game “Genesis” Estate | $1.5 million |

| CryptoPunk #4156 | $1.25 million |

| Forever Rose | $1.25 million |

| Rick and Morty “The Best I Could Do” | $1 million |

Most NFTs are sold through auctions, however, they might also have a “Buy Now” option which can be used if you have the required amount of Ethereum available – some might even have a fixed price.

How Do NFTs Work?

We understood what NFTs are and what purpose do they serve, but how do they work? What stands behind these NFTs? The answer to these questions is pretty simple – an NFT is a unit of data stored on the Ethereum blockchain. When you create an NFT, you are entitled to the creator of that particular NFT, meaning that you hold all the copyrights for it. Additionally, you have the right to duplicate it as many times as you want. Same as physical collectibles, the original NFTs are most often valued more than their replications and their price is heavily affected by supply and demand – the rarer the NFT, the higher its price.

Non-fungible tokens also provide the option for creators to receive royalties each time one of their NFTs is sold even after the initial sale. However, the percentage that they get is not universal; meaning that this option’s properties are different in each platform.

All in all, NFTs are tokens built on blockchain technology that allows people to tokenize visual and audible files and sell them on many platforms. To put it in simple terms, instead of getting a physical painting to hang on a wall, the collector/buyer gets a digital file that is exclusively his. This also means that NFTs can have only one owner at the same time.

How and Where to Buy NFTs?

In order to buy an NFT, you must first buy a cryptocurrency that goes by the name of Ethereum since these non-fungible tokens are mostly built on the Ethereum blockchain network. At the time of writing, Ethereum (ETH) is listed on nearly all of the major cryptocurrency exchanges, the most widely used being Binance, Gemini, Coinbase, Kraken, and Bitfinex.

After you get your hands on some Ethereum, you should do some background research on the NFT you are interested in buying. For example, if you are interested in buying and exclusively owning a video of Lebron James dunking on a particular game, the best option for you may be NBA Top Shot – a platform that is licensed by the NBA.

After you find the marketplace that suits your intentions, you are eligible to use your Ethereum tokens to buy the NFT of your choice; nevertheless, if the “Buy Now” option is not available, you can use your Ethereum to bid on the NFT’s price.

At the time of writing, there are dozens of NFT marketplaces, with some of the most prominent being:

- SuperRare – only single-edition digital artwork available.

- Foundation – known for being the marketplace that hosted the viral meme Nyan Cat’s initial sale.

- Mintable – is considered the eBay of NFTs; allows you to create your own NFTs for free.

- OpenSea – claims to be “the first and largest marketplace for user-owned digital goods”

- Axie Infinity – a Pokemon-inspired video game in which players can collect cartoon pets and battle other players.

- NBA Top Shot – an NBA-licensed platform that allows fans to collect and trade digital “moments” from NBA games.

- Nifty Gateway – a centralized U.S. dollar marketplace that collaborates with celebrities to create NFTs. It features works with Beeple, Garyvee, Forbes, Eminem, Playboy, and many more.

- Decentraland – a platform that claims to be “the first-ever virtual world owned by users.” It allows you to explore casinos, visions of space, and underwater kingdoms while developing land holdings and influence.

Where to Store NFTs?

In order to buy an NFT, you firstly need to create a wallet that is NFT compatible. While some platforms have their own integrated wallet where you can store the NFTs you buy or own, there are many marketplaces that require the use of an external wallet to store a non-fungible token. At the time of writing, these five are the leading wallets for storing NFTs:

1. Metamask

Pros:

- It is maintained by ConcsenSys, which is backed by the Ethereum Foundation

- User-friendly Interface

- Available on both mobile and PC

Cons:

- Primarily compatible with the Ethereum compatible blockchains

- Accused of sharing identifiable information to data collection networks

2. Trust Wallet

Pros:

- Founded by Binance, making it more credible

- User-friendly Interface

- Offers one-click access to DApps; including NFT applications

Cons:

- Only available on mobile

- Because it is affiliated with Binance, it promotes BNB network products ahead of Ethereum network products

3. Math Wallet

Pros:

- Backed by Binance Labs and Alameda Research

- Native support for multiple blockchains

- Ledger includes a Math Wallet integration which guarantees additional security of stored assets

Cons:

- Many reports from IOS users having issues with dApps

- Has many bugs; mainly because it is still being actively developed

4. Enjin

Pros:

- Includes a marketplace for trading these digital assets using their native token – ENJ

- Has an implemented customer support desk

- Their app includes advanced security features like biometrics and auto-lock

Cons:

- Only available on mobile

- Supports only Ethereum-based assets and NFTs

5. Alpha Wallet

Pros:

- Supports all Ethereum-based games and tokens

- Ideal interface for NFT beginners

- Directly supports marketplaces like OpenSea and game platforms like Dragonereum

Cons:

- Is an Ethereum-only blockchain wallet

- Only available on mobile

Creating Your Own NFT

As mentioned above, an NFT is basically a unique piece of digital art secured in the blockchain. Today, you can create your own NFT by a process known as minting. When you mint an NFT, it means that your digital art has become a part of the Ethereum blockchain. Minting an NFT can be done through these six simple steps:

- Create a wallet that supports NFTs (i.e. Metamask)

- Link that wallet to an NFT marketplace that provides the option to create NFTs (i.e. OpenSea or Mintable)

- Locate the “Create” or “Mint” tab

- Upload the file that you want to mint and fill in the information required (i.e. NFT name, description, and properties)

- Set the price and type of sale for your NFT (i.e. fixed price, auction, or auction with “Buy Now” option”

- Tap on “Create” or “List this item” and your NFT is ready for sale

Click here to create your own NFT through Mintable.

Click here to create your own NFT through OpenSea.

Takeaways

- NFTs is short for non-fungible tokens.

- Non-fungible tokens are tokens that are non-fungible – meaning that they are unique and cannot be replaced.

- NFTs are built on blockchain technology, making them very secure.

- NFTs are known as the collectibles of blockchain technology since they can have only one owner at a time.

- The variety of NFTs range from digital art pieces to game collectibles, to ownership of real estate.

- Most of the time, you can only buy an NFT using Ethereum.

- Some of the most famous NFT trading platforms are OpenSea, Foundation, Minteable, OpenSea, Decentraland, Nifty Gateway, NBA Top Shop, and SuperRare.

- Not all blockchain wallets support NFTs. However, some of the best ones that support NFTs are Metamask, Enjin, Math Wallet, Alpha Wallet, and Trustwallet.

- There are many platforms on which you can create your own NFT for free – with gas fees only applied after you sell that particular NFT. All you have to do is have some digital art and you are ready to go.